Ultimate Guide to Car Insurance in Singapore (2023)

24 Dec 2022 | Updated on 31 Dec 2022

Here's all you need to know to find the best insurance for your car: we help you understand the types of coverage, terms like NCD & excess, how they affect your premiums and more.

Types of Car Insurance in Singapore

Third Party Only (TPO) Car Insurance

Third Party, Fire and Theft (TPFT) Car Insurance

Comprehensive Car Insurance

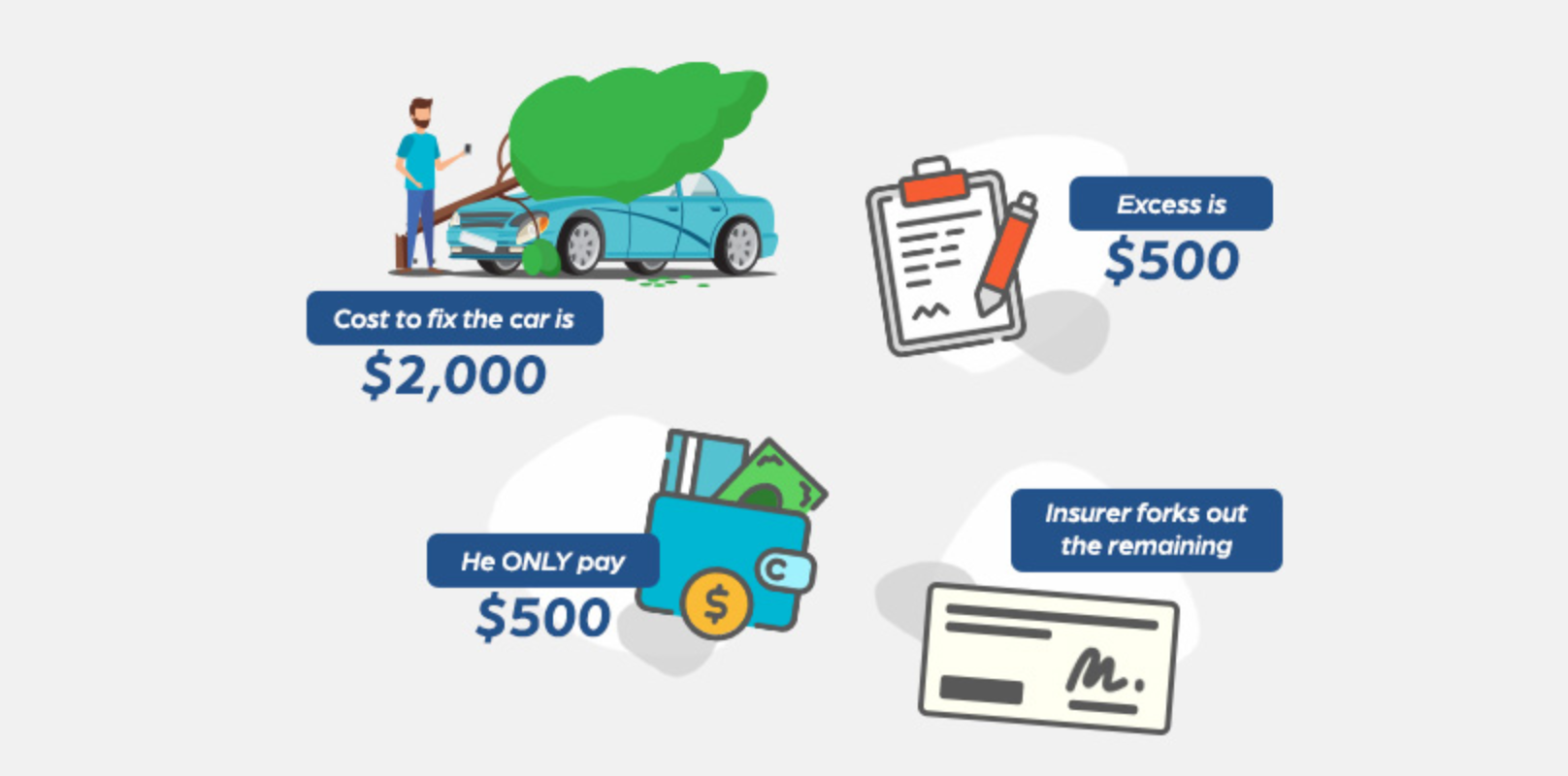

What is Excess?

Here's an example:

Here are the three types of excess in car insurance:

2. Excess in 'Third-Party': This excess applies to damages incurred by the third party. You may need to pay this on top of the excess in your ‘Own Damage’.

3. Excess in 'All Claims': This excess refers to the total sum payable to every accident, regardless of whose damages the excess covers.

Generally, opting for a higher excess helps lower car insurance premiums. However, with less insurance pay-out, you’re putting yourself at a higher financial risk on the roads.

No-Claims Discount (NCD)

Some drivers pay an additional fee for the NCD protector scheme. This allows them to make one claim and still retain their NCD privileges.

Your NCD is also transferable from one car to another. Even if your car is scrapped, you can retain your NCD for at least 12 months. On another note, if you own two cars, your second car might not enjoy the same NCD privileges as the first car.

Named Driver(s)

Family members are oftentimes added as named driver(s) to keep financial risks low. Should an unnamed driver get into an accident while using your car, the insurer can impose a higher excess on your claim.

11 factors that affect the cost of your car insurance in Singapore:

2. Age of car – The cost of car insurance generally decreases with the age of your car

3. Age of insured – People below the age of 30 and over the age of 65 can expect to pay more expensive premiums

4. Occupation – An outdoor job indicates that you will use your car more often and pose a higher risk of accident. This can translate to higher premiums

5. Marital status – Insurers may lower your car premium if you have a family to look after

6. Years of driving – Drivers with less than four years of experience will have to pay higher car insurance premiums

7. Type of car usage – Private-hire insurance premiums tend to be higher than policies for private vehicles

8. Driving accident claim history – a ‘loading fee’ applies if you have made a single claim of above $10,000 OR made two or more claims in the past three years

9. No claims discount – If you’ve been claim-free for a certain number of years, you’ll be rewarded with a renewal discount. Find out more about NCD here.

10. Honesty and integrity – Dishonesty about your driving history may cost you a higher premium if false information is provided

11. Car modifications – Modifications that are not LTA-compliant will require additional cover which will increase the premium price

Car Accident Checklist

Step 1: Assess the situation

• Lodge a police report for hit and run accidents, collision with vehicles not registered in Singapore and government property

Step 2: Ensure Safety

• Move your vehicle to the roadside to prevent traffic obstruction

• Place a hazard sign 50m away from the rear of your car

Step 3: Exchange Information

• Full Name of involved parties and witnesses

• NRICs of involved

• Contact numbers

• Home Addresses

• Insurer Details

Step 4: Gather Evidence

• The car accident scene and surrounding areas. (include lane markings, debris or prominent damage to structures)

• The licence plate numbers

• The car accident damages

• The time, date and location of the car accident

• The weather and road conditions of the car accident scene

Step 5: Assess Damage

Common mistakes to avoid when making car insurance claims:

2. Not seeking advice from insurer – Your insurer is your go-to when an accident arises. They’ll redirect you to a hotline, if any, and advise you on which workshops to go to.

3. Admitting to fault or liability – Agreeing to negotiate or making offers of private settlement means admitting liability. The involved party can use this against you to shirk responsibility from the accident.

4. Not getting the full picture – The less details you note down, the less likely your claims will be approved quickly. Here’s what you need to note down in a car accident

5. Submitting badly documented evidence – Usually, the insurer uses car camera footage to piece the story together. If you don’t have a car camera footage to submit as evidence, you’ll need many photos of differing angles. Try to get a good mix of close up, medium-range, and wide-angle shots.

6. Moving the vehicle unnecessarily – This affects your evidence documentation, for you may miss out crucial details and it gives the other party a chance to dispute your claims. If necessary, look for a witness.

7. Visiting an unauthorised workshop – Usually, the insurer uses car camera footage to piece the story together. If you don’t have a car camera footage to submit as evidence, you’ll need many photos of differing angles. Try to get a good mix of close up, medium-range, and wide-angle shots.

Best car insurance policies in Singapore for 2023

Sgcarmart

Get up to 20% off and $300 cashback when you renew with select car insurance!

- Auto comparison for your future renewal quotes

- We provide claims support for your accident claims

Car Insurance Advice

Top Car Dashboard Camera Choices to Consider in 2025

Why used car dealers love the Sgcarmart Warranty

Things to look out for when buying online car insurance

Comparing the different types of car insurance in Singapore

No Claims Discount - What is it and how does it affect me?

Understanding the types of car insurance in Singapore

Car sharing in Singapore: Let's talk about insurance for drivers

What should you do if someone steals your car overseas?

FAQ

Don’t assume that emergency assistance is easily available when car accidents occur. Some insurers don’t provide 24-hour emergency assistance and settling for unauthorised emergency services can complicate your claims process.