Cars here are invariably depreciating assets - but do we regain some ground when COE premiums skyrocket?

05 Mar 2022|49,489 views

Over the past couple of years, becoming engulfed in fury appears to have become the default reaction to the LTA's fortnightly Wednesday-afternoon announcements.

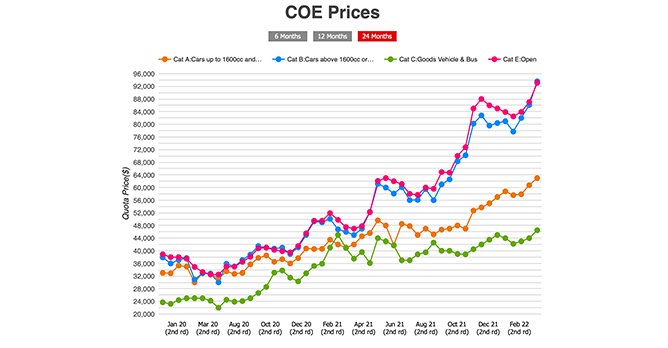

It's understandable - COE premiums are scaling heights that we haven't seen for at least six to nine years, depending on which category you prefer (or can afford) to shop in.

What's the story behind that?

Starters - back to the basics of supply and demand

We don't want to bore you with a topic that's constantly squeezed and wringed dry of its last drop, but here's a simple recap, theoretically, of how things work.

As COE premiums go up, a new car can start to look like a really bad value proposition, since more than half the money you're paying is based on an intangible cert moulded by the supply pressures of an artificially created system.

Finding no sense in giving in to a good battering from strong yet unnecessary financial headwinds, it's not uncommon for many to then turn to the used car market to stake the storm out. In turn, many second hand-dealers, cognisant of the increased demand, seize the opportunity to implement slightly steeper mark ups on the prices of their cars, knowing that these will boast lower annual depreciation rates in comparison anyway.

This is where the inquisitive, profit seeking ones among us come into the picture. If we assume that dealers see the possibility of implementing fatter mark-ups on the cars that they procure, we, as the owners of existing cars, should also see some of those extra margins coming back to us when we transact our cars with them.

And so - this is how the basic theory of higher COE premiums translating into higher resale values for cars goes. At least theoretically.

But if you need a car… you still need a car

There's a pretty good chance that many among us who are seeking to sell our cars at a profit now still want to drive. Where, then, would we procure a new set of wheels from?

Surely not the new car market.

And so, we return to the second-hand market… in which we find cars that would have higher dealer mark-ups than, say, two-and-a-half years ago. That higher profit margin that you may have just enjoyed from the sale of your own car? That probably applies to the other used car you're now considering as well.

While the rise may translate on first glance into a fantastic leap in profits, the reality is that everything has become inflated. And if this happens to be your only property, you'll still need somewhere to stay, meaning that you're not really earning as huge a margin as you might imagine once the shifting is done and dusted.

Cars, of course, don't mirror properties since it's highly unlikely (not impossible) for them to appreciate in value. But the notion of a uniform, market-wide increase holds in the current COE premium climate.

COE premiums have always fallen on a spectrum - a strict expensive vs inexpensive binary doesn't exist

Someone looking at the current climate will reminisce fondly on the good old days when Category A was well within $40,000. But in recent memory, premiums actually dropped to as low as $23,000 during the bidding round of 5 December 2018 (Category B stood at $31,000 at that point, against the current $88,000).

Of course - given the fact that most of us normally lock the deal in as long as the price is good enough, it's impossible to have the prescience of exactly when premiums are at their lowest. Nonetheless, what this means is that even in the 'pre-spike era', buying your car - brand new - at the right time would have reaped you significant savings over someone that had made the purchase just a few months earlier or later.

The Toyota Corolla Altis Elegance cost just $95,988 in May 2019, which translates into a depreciation of $8549 per year, assuming an ARF of $21,000. Just a few months earlier in Dec 2018, however, the same car cost $91,988, translating to a depreciation of $8149 per year.

Which brings us on to our next point…

Who will rising COE premiums ultimately benefit?

A quick scan of Used Car listings shows that Elegance variants of the Corolla Altis sold between the late-2018 to mid-2019 currently retail with annual depreciations ranging from $9,500 to above $10,000.

While the mark-up is already evident, these are nonetheless still significantly lower figures than $12,000-ish annual depreciation for a brand new Corolla Altis Elegance - its new platform, tech and features notwithstanding, naturally.

That's the first part of the picture. The second part, of course, concerns your next course of action after selling your car.

But those who are seeking to downgrade their vehicle (from a mid-size SUV to a compact hatchback, perhaps) may also channel the slightly fatter margins to their next second-hand, or even brand new purchase. Think of it as slightly better cashback, rather than actual profit-making.

Naturally, with the used car market it's often important to remember that demand (and thus, the asking price) tends to fluctuate across different models. Evergreen cars that have wide-reaching appeal stand to gain more, as well as cars that fall within certain niches - like the turbocharged Honda Civic Hatchback (both the 1.0-litre engine and 1.5-litre engine ones).

A reiteration - it's more likely you'll mitigate depreciation than be gifted a life-changing windfall even during this period

But as we've mentioned, caveats still remain. The most important is the same reality of car-ownership in Singapore: there's no changing the status of cars as financial liabilities. Only the degree of depreciation tends to oscillate, and while that's certainly pointed in our favour currently, proceeding with caution is still necessary.

Of course, don't take this as a sign not to try - you'll never know how much your car can fetch till you actually put it out there on the market.

If you're not looking to part ways with it, then - as they say - keep scrolling (er, actually, we're done). If you are, then there are many ways in which you can sell your vehicle, such as getting a best-price valuation through Quotz, listing it on our Used Cars platform, or finding an agent to consign it for you.

Sgcarmart Quotz

Sell your Car for the Best Price

Simply Sell Your Car for MORE!

- Auction to 500+ dealers

- Confirmed price, No reductions

Here are some related articles that might interest you

Tips to get the best price when selling your car to used car dealers!

Car Consignment 101: How to sell your car

Should you sell your car and switch to taking public transport?

How to fetch a higher price for your used car when selling it to a dealer

6 simple things you can do to sell your car for the highest price

Over the past couple of years, becoming engulfed in fury appears to have become the default reaction to the LTA's fortnightly Wednesday-afternoon announcements.

It's understandable - COE premiums are scaling heights that we haven't seen for at least six to nine years, depending on which category you prefer (or can afford) to shop in.

What's the story behind that?

Starters - back to the basics of supply and demand

We don't want to bore you with a topic that's constantly squeezed and wringed dry of its last drop, but here's a simple recap, theoretically, of how things work.

As COE premiums go up, a new car can start to look like a really bad value proposition, since more than half the money you're paying is based on an intangible cert moulded by the supply pressures of an artificially created system.

Finding no sense in giving in to a good battering from strong yet unnecessary financial headwinds, it's not uncommon for many to then turn to the used car market to stake the storm out. In turn, many second hand-dealers, cognisant of the increased demand, seize the opportunity to implement slightly steeper mark ups on the prices of their cars, knowing that these will boast lower annual depreciation rates in comparison anyway.

This is where the inquisitive, profit seeking ones among us come into the picture. If we assume that dealers see the possibility of implementing fatter mark-ups on the cars that they procure, we, as the owners of existing cars, should also see some of those extra margins coming back to us when we transact our cars with them.

And so - this is how the basic theory of higher COE premiums translating into higher resale values for cars goes. At least theoretically.

But if you need a car… you still need a car

There's a pretty good chance that many among us who are seeking to sell our cars at a profit now still want to drive. Where, then, would we procure a new set of wheels from?

Surely not the new car market.

And so, we return to the second-hand market… in which we find cars that would have higher dealer mark-ups than, say, two-and-a-half years ago. That higher profit margin that you may have just enjoyed from the sale of your own car? That probably applies to the other used car you're now considering as well.

While the rise may translate on first glance into a fantastic leap in profits, the reality is that everything has become inflated. And if this happens to be your only property, you'll still need somewhere to stay, meaning that you're not really earning as huge a margin as you might imagine once the shifting is done and dusted.

Cars, of course, don't mirror properties since it's highly unlikely (not impossible) for them to appreciate in value. But the notion of a uniform, market-wide increase holds in the current COE premium climate.

COE premiums have always fallen on a spectrum - a strict expensive vs inexpensive binary doesn't exist

Someone looking at the current climate will reminisce fondly on the good old days when Category A was well within $40,000. But in recent memory, premiums actually dropped to as low as $23,000 during the bidding round of 5 December 2018 (Category B stood at $31,000 at that point, against the current $88,000).

Of course - given the fact that most of us normally lock the deal in as long as the price is good enough, it's impossible to have the prescience of exactly when premiums are at their lowest. Nonetheless, what this means is that even in the 'pre-spike era', buying your car - brand new - at the right time would have reaped you significant savings over someone that had made the purchase just a few months earlier or later.

The Toyota Corolla Altis Elegance cost just $95,988 in May 2019, which translates into a depreciation of $8549 per year, assuming an ARF of $21,000. Just a few months earlier in Dec 2018, however, the same car cost $91,988, translating to a depreciation of $8149 per year.

Which brings us on to our next point…

Who will rising COE premiums ultimately benefit?

A quick scan of Used Car listings shows that Elegance variants of the Corolla Altis sold between the late-2018 to mid-2019 currently retail with annual depreciations ranging from $9,500 to above $10,000.

While the mark-up is already evident, these are nonetheless still significantly lower figures than $12,000-ish annual depreciation for a brand new Corolla Altis Elegance - its new platform, tech and features notwithstanding, naturally.

That's the first part of the picture. The second part, of course, concerns your next course of action after selling your car.

But those who are seeking to downgrade their vehicle (from a mid-size SUV to a compact hatchback, perhaps) may also channel the slightly fatter margins to their next second-hand, or even brand new purchase. Think of it as slightly better cashback, rather than actual profit-making.

Naturally, with the used car market it's often important to remember that demand (and thus, the asking price) tends to fluctuate across different models. Evergreen cars that have wide-reaching appeal stand to gain more, as well as cars that fall within certain niches - like the turbocharged Honda Civic Hatchback (both the 1.0-litre engine and 1.5-litre engine ones).

A reiteration - it's more likely you'll mitigate depreciation than be gifted a life-changing windfall even during this period

But as we've mentioned, caveats still remain. The most important is the same reality of car-ownership in Singapore: there's no changing the status of cars as financial liabilities. Only the degree of depreciation tends to oscillate, and while that's certainly pointed in our favour currently, proceeding with caution is still necessary.

Of course, don't take this as a sign not to try - you'll never know how much your car can fetch till you actually put it out there on the market.

If you're not looking to part ways with it, then - as they say - keep scrolling (er, actually, we're done). If you are, then there are many ways in which you can sell your vehicle, such as getting a best-price valuation through Quotz, listing it on our Used Cars platform, or finding an agent to consign it for you.

Sgcarmart Quotz

Sell your Car for the Best Price

Simply Sell Your Car for MORE!

- Auction to 500+ dealers

- Confirmed price, No reductions

Here are some related articles that might interest you

Tips to get the best price when selling your car to used car dealers!

Car Consignment 101: How to sell your car

Should you sell your car and switch to taking public transport?

How to fetch a higher price for your used car when selling it to a dealer

6 simple things you can do to sell your car for the highest price

Photos by Editorial Team, Unsplash/Jason Leung, shawnanggg

All Advice Categories

Related Motor Directory Categories

Tags

Products & Services

For Owners

Quick Links

About Sgcarmart